Zooming In Zoom

There are start-ups that solve a new use case and then there are start-ups that address an existing use case in a better way. Founded in 2011 by ex-VP of Webex, Eric Yuan, Zoom is part of a later category. Here is how Zoom defines its mission and vision:

Our mission is to make video communication frictionless…Our goal is to make Zoom meetings better than in-person meetings. …Our vision is to empower people to accomplish more through video communications.

The keyword here is video communication. It’s not just generic communication that encompasses chat, messaging, email, audio. This precisely is the difference between new age SaaS companies and tech companies of the previous era. The companies of the previous era bundle various services and use distribution as a moat to push other services. Today it’s different. There are two reasons for it:

The end customer is a user today. With the bottom-up approach, customers want the best of the breed. For companies, it allows a singular focus to build a product that solves one use case better than anyone else.

API integrations with other tech companies (solving different use case) allow integrating with other best of breed start-ups that solves adjacent use cases. I mentioned about Network effect of Okta in the article here:

Since Okta was built for the cloud, it ensured that it had integrations with the majority of cloud applications. New customers came because of these integrations. Since these customers were using Okta, the new cloud business wanted to ensure that their applications had Okta integration. Hence further integrations. It led to a network effect.

From a product standpoint, the differentiator for Zoom is its user experience. It just works. The main reason for it is the video-first and cloud-native approach taken from day 1. It was different than a traditional legacy provider (Webex) that added video over the top of an existing chat or audio tool. As mentioned in the S-1 report:

We developed a proprietary multimedia router optimized for the cloud that separates content processing from the transporting and mixing of streams. Our globally distributed cloud architecture delivers a differentiated user experience.

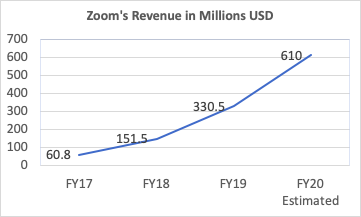

Growth

In a span of 9 years, Zoom now has estimated revenue for the coming fiscal year as about 609-610M USD with over 2400 employees. As on Q3FY20, customer count is 74100 with overall 546 customers paying more than 100K USD revenue annually.

The interesting thing about this growth is that the new customers accounted for 61% of the year to year growth while 31% of new revenue is coming from an existing customer. Now, why is this good? Zoom model like many other tech startups (Slack, DropBox)is based on a bottom-up approach. And at the scale of 500M USD if still, the sizeable revenue is coming from new customers, then it goes a long way to show the total addressable market.

To put things in perspective:

Consider a hypothetical SaaS company with 100 customers having an average ARR of $30K.Let the average maximum potential ARR from each customer be $100K. The total addressable market just from existing customers becomes $10M.And $3M out of which is already captured. To capture the remaining $7M, all you need is to scale fast to avoid fragmentation. *

This could be one of the reasons why Zoom is hiring enterprise sales rep aggressively in the last 12-18 months. Another reason being international expansion. In Q3FY20, APAC and EMEA revenue combined grew 98% year-over-year and represented approximately 20% of revenue. Revenue from the Americas was up 82% year-over-year and represented approximately 80% of revenue.

Net expansion rate:

Zoom is one of the few SaaS start-ups that has a Net expansion rate of over 130% consistently in the last few quarters. What it means is: If on an average customer invested 50K last year in a Zoom product, it invests 65K this year.

In fact, because of the low churn rate, Zoom doesn’t incentivize their customer or their sales reps for moving their monthly customer to an annual plan.

Partnership & Marketplace:

Last year Zoom partnered with Verizon to resell Zoom solution to its SMB market. Verizon already has a partnership with Cisco Webex for Enterprise customers.

The marketplace will be a major driver to focus on vertical use cases specific to particular industries. Currently, Zoom has over 150 + integrations across various categories.

Focus on most of these integrations is that while the customer is using a particular platform, they can launch the zoom app and start a video conferencing call while staying on the same platform. As Eric rightly mentioned in one of the calls, the idea is that customers shouldn’t feel that they are using two different platforms.

Example:

Sales rep making a call while using Salesforce* and transcript from the Zoom meeting is recorded within Salesforce.

Launching a Zoom call within your existing workflow in Jira, Slack, DropBox, and other platforms.

Overall Market:

Market at which Zoom plays comes under Unified Communication and Collaboration. As per IDC, it is estimated to reach $43 billion by 2021. Zoom focuses on Video within that segment. There are various players like legacy web-based meeting providers: Cisco Webex and Skype for Business (now Microsoft Teams); bundled solutions providers with basic video functionality, like Google Hangouts; and point solutions providers like BlueJeans and others.

There are new-age companies that cater to similar use cases in a different way. Examples:Loom: Sending short videos to share messages instead of waiting for meetings, Yac.Chat: Only Voice collaborations for remote teams and, Tandem.

Video as a mode of communication is bound to grow with remote teams and use cases across different industries like healthcare, education, government, and others. Interesting times ahead to see how Zoom maintains this growth trajectory.

*Salesforce was one of the major investors in Zoom.

*For the sake of simplicity, we have not divided the numbers into Enterprise, Mid Market and SMB.