Plaid & Visa

For a start-up that got started in 2012, was in private beta till 2015, to get acquired by Visa at 5.3 B USD in a span of 5 years is quite an achievement. Founded by two former Bain associates, William Hockey and Zach Perret: the initial idea for Plaid founders was to launch a fintech application. However, in the process, founders encountered a major opportunity in building the infrastructure that can serve other fintech applications. Hence chose to become an enabler for other financial technology startups.

Today, Plaid highlight below as their mission & vision:

Mission: Make money easier for everyone.

Vision: Democratizing financial services through technology. Plaid build beautiful consumer experiences, developer-friendly infrastructure, and intelligent tools that give everyone the ability to create amazing products that solve big problems.

What exactly is Plaid?

Plaid provides APIs that let developers connect to bank accounts of their users and access data related to it.

If I need to create an app that offers better interest rates to international students not just based on the academic profile but also other factors like current financial status and willingness to pay. I have two options:

I will ask each user to provide all the banking data manually on my app.

or I make an API connection or use other technology that connects to all the banks across the country and gets permission from users to retrieve that data.

The first one is not a neat approach. Bad user experience may lead to a drop in # of users completing the workflow. This impacts revenue directly.

The second one is not feasible for a small start-up. Having integration with so many banks (large, small, credit unions) will require both time & capital. Each bank will have a different approach for authenticating users, retrieving data, presenting data, etc. Further, I have to build out a team (technical, legal, compliance) that is tasked for only ensuring that integration with all the banks works all the time.

That’s where Plaid comes in. It has integrations with most of the major banks in the US and has recently launched in the UK as well.

So how it works?

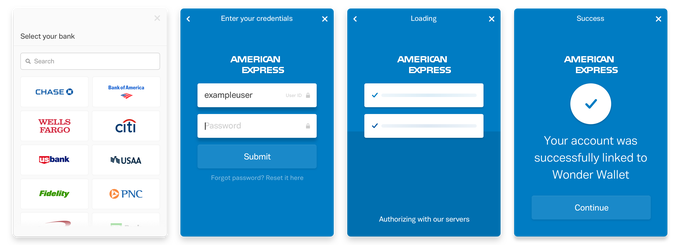

Within an app, users can select their bank and provide the login credentials as seen on screen 2 of the below image. Plaid code in the app captures that information and shares it with the bank.

Source: Plaid (Image 1)

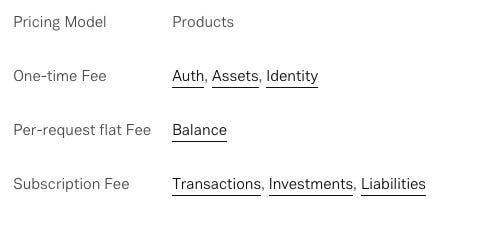

Plaid has multiple products like Identity, Transactions, and others that may serve various use-cases like:

Verify the identity of the end-user to reduce fraud, use the account holder’s information like name, email address, phone, etc. : Identity

Summarize all the spendings category by retrieving transaction details of different accounts like credit, depository accounts: Transactions

or If I am focussing on building an app that offers credits for a particular segment of customers not targeted efficiently by a traditional large bank, I may want to know their current assets and overall liabilities. This can be done by-products like Assets and Liabilities.

Source: Plaid Products, (Image 2)

There are similar products for Investments (get info about securities holding) and Balances (real-time balance of your account).

It’s all straightforward till now. But remember we are talking about Banks here. How is Plaid doing all this so easily? It actually does integration using various methods like OAuth for authorization, Durable API, OFX, and others for transmission. In some cases, these methods also include screen scraping.

An important point to note here is that screen 2,3 and 4 in Image 1 is not an American Express web page. It’s actually Plaid’s UI. As a user, I may not be fully aware that what level of information is being shared. Plaid does display a pop-up that says you’re sharing data with Plaid and there is a privacy term if as a user you actually read it.

{kind=link}

Growth:

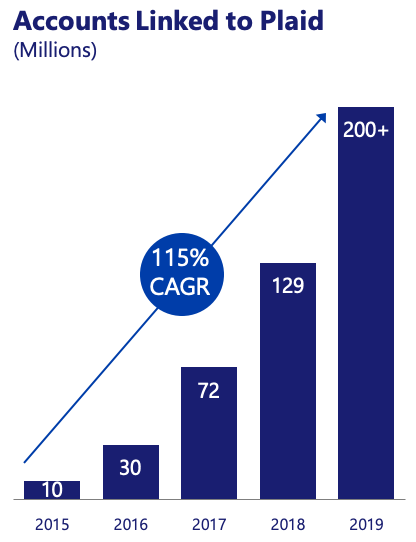

Plaid is currently powering 80% of the largest fintech apps in the US. Growth for onboarding fintech apps has been exponential as seen below.

Source: Visa

Plaid understood that its growth will always be a function of the overall fintech space. As new use cases emerge, more start-ups will be using Plaid as their backend infrastructure. Hence you see them come up with annual Request for Start-ups (RFS) ideas that can build on top of Plaid’s infrastructure. RFS: 2017,2018, and 2019.

Most of the growth has been organic until 2019. Plaid got last round (Series C) funding of 250M USD in December 2018 with a valuation of ~2.5B USD. It included quiet funding from both Visa & MasterCard.This was used to fuel inorganic growth, Plaid acquired Quvo in January 2019 for 200M USD. It was to expand the product portfolio to investments in addition to lending.

Understanding where Plaid is heading will be incomplete without deep-diving into two things:

Open Banking

Synergies with Visa and it’s business model.

Open Banking:

Open Banking is a practice/regulation that asks Banks to allow access to the customer’s data (like transactions , accounts ,lending frequency etc ) with third-party financial services providers.This will be done at done at the behest of customers.

The idea is that the bank is the custodian of that data and the customer is a true owner. She can consent to share her banking data with other providers that helps create better financial services/applications. Data sharing will be usually done through APIs.

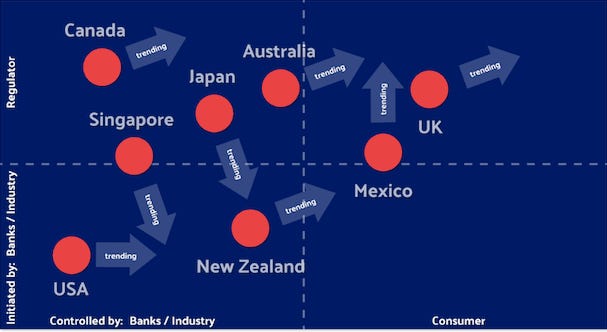

Each country has its own approach to open banking based on their markets. Some like EU, UK have a regulatory approach while others like the US have taken a market-led approach. Both EU’s PSD2 (Revised Payment Service Direction) and the UK’s Open Banking Limited is pretty much setting the benchmark. Australia has open banking as part of Consumer Data Rights hence it’s broader than just financial framework. The US has a market-led approach because of the fragmentation of markets. It is one of a market where screen scrapping is prevalent because of no standard framework. India has made it in two-phase: one with relations to payments (UPI) and others in relation to account-level data through aggregators (limited progress so far).

Source: Open Data Institute

So Open Banking will be implemented across the countries at some point.

But why is it important in the context of Plaid?

Open Banking as we see is a push for enabling innovation in the fintech ecosystem. Plaid has fast forward the reality in the US that Open Banking envisage. They have done it without proper regulation in place. Hence it may not have the high standards of consent and privacy mechanism that we may see when Open Banking will be in full effect.

Part of the reason is the situation of the banks in the US. Banks had their reservations in partnering or sharing the data. These reasons can be attributed to the following:

There is no clarity on what the Banks are getting in return from fintech apps in exchange for sharing the data. (Reciprocity)

While allowing fintech apps access to customer data, are banks also sharing liabilities with new start-ups in the event of a data breach?

Most of the banks in the US including small banks, credit unions don’t have the technology to support APIs to third parties. These banks are using core solutions provided by a few dominant players like Fiserv, Jack & Henry, FIS, and Finastra of the world. Banks have limited negotiating power with these core solution providers.

Plaid started integration with few banks but now has a partnership with over 11000 banks. In fact, it now sees requests coming from banks to integrate with Plaid. These are banks that are compelled for a partnership to ensure they retain their existing customers who want to use new fintech apps. The only way for banks to do that is by partnering with Plaid.

Revenue Model

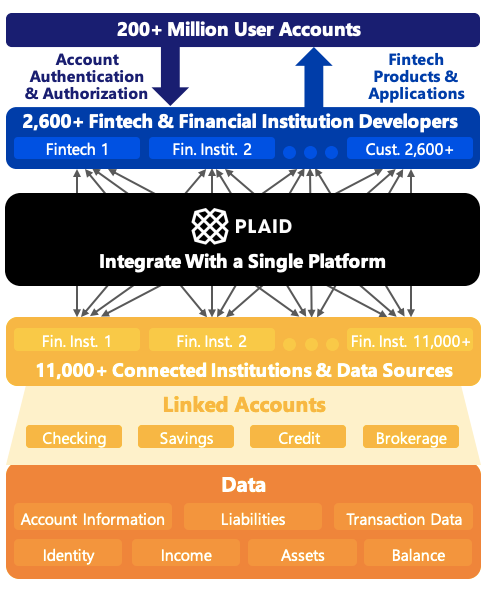

Plaid sits between banks & fintech apps in the ecosystem. It’s part of the network that can be viewed as a microcosm of a large network that Visa or Master Card enjoys.

Source: Visa’s acquisition of Plaid.

Plaid’s revenue model is based on APIs, it charges application teams either based on per API request (volume), subscription (flat-recurring), or one-time based on the product selected.

Source: Plaid Billing

This model should be a major factor that got Visa or MasterCard interested in Plaid. Let’s see why.

Visa

As per the 2019 annual report, a major part of Visa’s revenue (68.5% of overall 29.2B USD) can be put into below two buckets, both of which are based on either total $$ flow or # of transactions within Visa’s network :

Service Revenues:

Visa earns a percentage of revenue from the banks for $$ (Gross Dollar Value) flowing through the Visa network.

It earned 9.7B USD on 8.8T USD transactions in 2019 (~0.001%)

Data Processing *

Based on a flat fee on the number of transactions done within the Visa network.

It earned 10.3B USD on 138B transactions in 2019. (~0.07 USD per transaction)

The commonality is that both Visa and Plaid, benefits as more money and data flows through their network.

The acquisition of Plaid will give access to Visa for keeping a tap on emerging start-ups that can be potentially acquired. Further, there will a synergy to expand the overall target market for both Plaid and Visa. But what’s most interesting is synergies in the analytics space. Visa has Consulting & Analytics arm used to provide insights on consumer trends based on transaction data. As the entire ecosystem move towards Open Banking, Plaid will not keep its role limited to the accessibility of data, as they highlighted:

We started out by building the technical infrastructure APIs that connect consumers, traditional financial institutions, and developers. Today, we add key insights to the data access we provide with our suite of analytics products.

Looking forward to seeing how things unfold as Plaid expands in other countries outside the US and the UK leveraging Visa’s reach.

*It includes revenue from other services as well.

*As of 13th Jan 2021 Visa and Plaid have decided to mutually terminate the merger.